How E-commerce Marketplaces in Pakistan Can Automate Vendor Payments

TL;DR: What You'll Learn

- The 5 categories of vendor payout channels available in Pakistan today are not just the two wallets everyone names

- Why manual payouts break around 50–100 active vendors, and the operational cost of waiting too long to automate

- How to match the right channel to each vendor type (registered SME, individual reseller, freelancer, international supplier)

- What T+0 vs T+1 vs post-return-window settlement does to vendor cash flow and marketplace risk

- Why API-based disbursement is the right architecture for marketplaces specifically, and where file-based flows still fit

- According to the SBP's FY25 Annual Payment Systems Review, retail payments reached 9.1 billion transactions worth PKR 612 trillion, with digital channels accounting for 88% of all retail transactions. The rails to automate against are mature. (SBP)

Running an e-commerce marketplace in Pakistan means paying vendors every settlement cycle across bank accounts, mobile wallets, and increasingly, EMI apps your finance team has barely heard of. Manual transfers work for ten sellers and fall apart at a hundred. This guide breaks down how to automate e-commerce marketplace payout workflows in Pakistan, including the channel landscape, settlement design, and the disbursement architecture that actually scales.

Where it helps, we'll show how our single-API approach, Simpaisa, solves the multi-rail problem most marketplaces hit by year two.

What Vendor Payouts Actually Look Like in a Pakistani Marketplace

A marketplace is a two-sided business: buyers pay the platform, and the platform owes sellers. The disbursement side moves net money, gross sale minus commission, refunds, shipping recovery, and withholding tax to each vendor's preferred channel. For one platform, this can be straightforward. For Daraz alone, it means handling 34,500 sellers and 88 logistics centers, with 48% of transactions completed through electronic payments in Pakistan. Most Pakistani marketplaces sit somewhere between those extremes, and most underestimate how fast the payout side gets complicated. Ce

Why Manual Vendor Payouts Break Past 50 Sellers

Most marketplaces start the same way. Friday morning, finance opens a Google Sheet, exports vendor balances, and types IBFT transfers into corporate net banking one by one. It works until it doesn't.

The breakdown is operational, not just time-based:

- Reconciliation drift. Every manual transfer creates a separate bank reference, and matching them back to orders, commissions, and refunds turns into multi-hour weekly work.

- Error rate climbs. Wrong account numbers, off-by-one decimals, duplicate transfers. One bad payout takes days to recover.

- Vendor disputes spike. Without a transparent breakdown of each payout's math, sellers question your commissions constantly.

- Cash-flow blindness. Finance can't forecast outflows accurately or hold rolling reserves against chargebacks.

- Audit gaps. Manual flows don't produce the trail SBP and tax authorities expect at scale.

Marketplace research consistently shows 62% of sellers abandon a marketplace if competitors offer faster payouts. In Pakistan's increasingly seller-mobile market, payout friction is a churn lever. Usedots

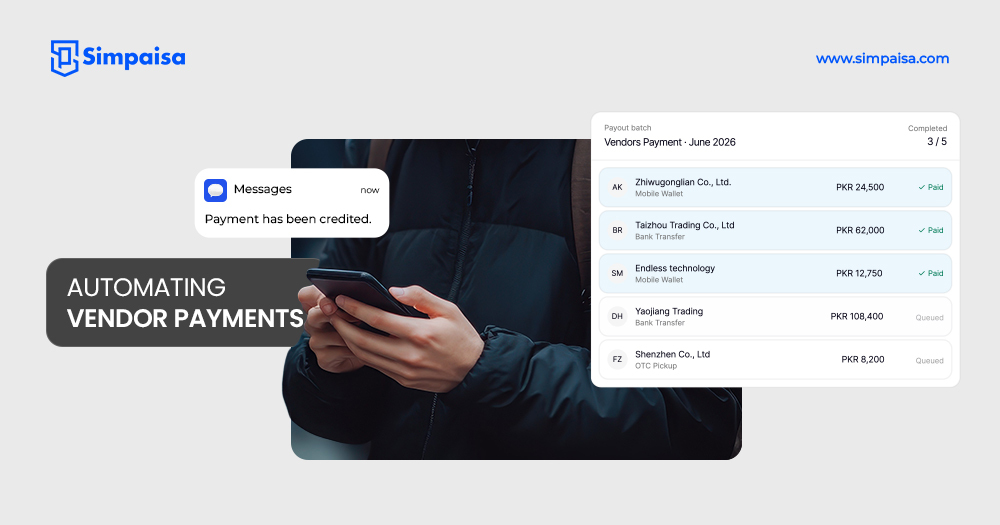

The Anatomy of an Automated Vendor Payout Workflow

An automated payout system, or what's often called a mass payment solution, Pakistan operators now expect, is built from six layers stacked together:

- Vendor master + KYC: single source of truth for CNIC/NTN, registered bank/wallet, tax status, active/suspended flag.

- Ledger: running record of earned, deducted, held, and payable balances per vendor.

- Payout schedule: eligibility rules: instant, daily, weekly, or post-return-window.

- Channel routing: logic that picks bank, wallet, or EMI per vendor based on preference and amount.

- The disbursement engine: Is the actual mechanism that triggers the transfer (file or API).

- Reconciliation & reporting: auto-matched success/failure, per-vendor statements, finance exports.

The next sections unpack the two layers that drive most of the design decisions: which channels you support, and how you trigger payouts.

Vendor Payout Channels Available in Pakistan

Pakistani vendor payment options fall into five broad categories. A marketplace doesn't need all of them, but understanding the full landscape helps you decide which ones matter for your seller mix.

1. Digital Wallets & Fintech Apps (preferred for fast payments)

The largest category by reach. JazzCash had 48 million registered users and 19.7 million monthly active users as of the end of December 2024, with 122,000 active agents and 350,000 active merchants. Easypaisa crossed 10 million active users and secured Pakistan's first digital retail bank license in January 2025. Beyond the two giants, the EMI category JazzCash, EasyPaisa, NIFT ePay, UPaisa, NayaPay, SadaPay, UBL Omni, Konnect by HBL, and Zindigis are now mature, with SBP-licensed wallets like NayaPay, SadaPay, and Finja widely used by freelancers, students, and Gen-Z sellers. For most marketplaces, this is the default payout channel for individual vendors. TMForum - InformNORBr

2. Digital Payment Gateways (PSPs) & APIs

Payment Service Providers consolidate multiple rails behind a single integration. Instead of building separate connections to JazzCash, Easypaisa, IBFT, and individual EMIs, a marketplace integrates one PSP and routes payouts through it. The PSP handles channel-specific authentication, retries, and reconciliation. This is the category most modern marketplaces standardize on once they pass 100+ active vendors.

3. Bank-Based Payout Solutions

Direct bank transfers via 1LINK's IBFT remain the backbone for registered SME vendors. 1IBFT is a 24/7 real-time service that ensures online transaction processing instantly across different banks, and SBP rules keep IBFT free up to PKR 25,000 per month per account, with banks allowed to charge 0.1% or PKR 200 (whichever is lower) above that. Larger payouts to incorporated suppliers, B2B partners, or logistics providers typically run through bank rails. Some marketplaces also use corporate disbursement tools offered directly by banks, but these usually require manual file uploads. 1LINKPide

4. International / Freelancer Payout Channels

For cross-border sellers, a Pakistani-owned marketplace paying international suppliers, or platforms serving Pakistani freelancers who happen to be vendors, the channel set widens to Payoneer, Wise (where supported), SWIFT wires, and increasingly EMI virtual cards with Mastercard/Visa networks. Pakistan's freelance market is estimated at 1.15 million freelancers earning over $1 billion per year, and marketplaces that overlap with this segment need a payout strategy that crosses borders cleanly. ffnews

5. Other Channels

QR-based payouts, payment links sent via SMS or WhatsApp, prepaid cards, and, for legacy reasons, physical cheques. These cover edge cases: a vendor temporarily without a working bank account, one-off payments to non-registered suppliers, or vendor rebates that need a quick, disposable channel.

How to Match the Right Channel to Each Vendor Type

The practical rule: let vendors choose their channel at onboarding and store it in the vendor master. Forcing every seller into a single rail is the fastest way to lose 20–30% of your marketplace to competitors who let sellers pick.

Settlement Cycles, Hold Periods, and Rolling Reserves

Settlement timing is where finance risk and seller experience collide:

- T+0 (same-day): highest seller satisfaction, highest marketplace risk if returns spike

- T+1 to T+3: industry standard for most product marketplaces; brief verification window

- Post return window (T+7 to T+14): safest for fashion, electronics, high-return categories, but creates seller cash-flow pain

Many platforms run a rolling reserve, holding back 5–10% of every payout for 30–60 days against future disputes. Category mix, refund rate, and dispute frequency should drive the model, not a one-size-fits-all default.

File-Based vs API-Based Disbursement: Why Marketplaces Should Default to API

Two ways to trigger automated disbursements, and for marketplaces specifically, one of them is clearly better.

File-based disbursement (CSV upload, sFTP drop, dashboard import): the disbursement platform processes a batch and returns a result file. Fits predictable, periodic flow/payroll runs, fixed-cycle vendor settlements, and monthly accruals.

API-based disbursement (REST call per payout, webhook on completion): your platform code triggers a payout the moment a vendor becomes eligible. Fits event-driven flows:

order confirmed → return window closed → payout fired.

Marketplace operations are inherently event-driven. Orders close at different times, return windows expire at different times, and refunds happen on no schedule. A file-based workflow forces marketplaces to artificially batch what should be continuous, which means vendors wait longer than necessary, and finance does extra reconciliation work. For e-commerce marketplaces, API-based disbursement is the right architecture, not a "nice to have." File-based remains useful for payroll-style flows where everyone is paid on the same cadence.

This is where a single-API approach pays off twice:

Simpaisa's disbursement API handles bank, JazzCash, and Easypaisa rails through one integration, and for marketplaces that want to consolidate further, the same Simpaisa integration covers payment acquiring from buyers, too. One vendor, one contract, one integration for both sides of the marketplace.

Compliance and Security Baseline for Marketplace Payouts

Any e-commerce marketplace payout Pakistan workflow has to clear three compliance layers:

- The SBP framework payments in Pakistan are regulated by the State Bank of Pakistan. A compliant disbursement partner operates within that framework either as a licensed PSO/PSP or through regulated partnerships with licensed financial institutions, so your payout flows stay auditable.

- AML/CFT + KYC vendor onboarding must capture CNIC/NTN, verify account ownership, and screen against sanctioned-party lists.

- Data security certifications like PCI DSS (for handling card and account data) and ISO 27001 (for organization-wide information security). Both are now expected, not optional.

Simpaisa is PCI DSS v4.0.1 and ISO 27001:2022 certified, operating under regulated partnerships and following SBP guidelines, giving marketplaces a trust layer that's expensive to build internally.

How to Choose a Disbursement Partner for Your Marketplace

A practical evaluation checklist:

- Multi-channel coverage through a single API: bank IBFT + major wallets + EMI partners.

- API-first architecture with file-based as a fallback, not the primary mode.

- Reconciliation depth: per-vendor settlement statements, transaction references, finance-friendly exports.

- Failure handling: built-in retry logic, structured error codes, and an exceptions queue.

- Compliance posture: PCI DSS, ISO 27001, and operating within SBP's regulatory framework are non-negotiable.

- Onboarding is designed to go live without complexity. The right partner should not require months of integration work.

- Transparent pricing: per-payout fees, channel costs, and monthly minimums stated upfront.

Expert Insight: The Single-API Question Most Marketplaces Don't Ask Early Enough

The conversation marketplaces should be having at month six is not "which wallet do we add next," it's "how many separate integrations are we willing to maintain?" Every additional rail you wire up directly adds engineering time, breaks during the next API change, and complicates your audit story. The marketplaces that win year three are the ones that picked a single API for disbursement (and ideally for acquiring too) early, then spent their engineering hours on actual marketplace features instead of payment plumbing.

Conclusion

The honest read on the e-commerce marketplace payout Pakistan automation: the channel landscape is mature, the rails work, and the technology is no longer the bottleneck. Three things decide success: cover the five channel categories properly with a vendor-selectable model so sellers stay; design event-driven settlement around an API-based disbursement workflow, because file uploads will never fit how marketplace orders actually close; and choose a single partner PCI DSS and ISO 27001 certified, operating within SBP's regulatory framework that consolidates the rails behind one integration, ideally one that also handles your buyer-side acquiring, so your engineering team integrates once for the full marketplace money flow.

Simpaisa is built around exactly this profile: PCI DSS v4.0.1 and ISO 27001:2022 certified, operating under regulated partnerships and following SBP guidelines, with a PSO licence application filed with the State Bank of Pakistan.

Ready to automate vendor disbursements? See how Simpaisa's single-API disbursement infrastructure covers bank, JazzCash, Easypaisa, Alfa, and HBL Konnect rails for Pakistani marketplaces, or talk to a disbursement specialist to map your current workflow.